Switzerland as a business hub

Trust in banking: what really matters

Trust in banking: what really matters

The reputation of Swiss banks has suffered since the bailout of Credit Suisse – yet the Swiss continue to place their trust in their local bank. Brand expert Stefan Vogler and Markus Boss, CEO of Regiobank Solothurn AG, know the secret to success: a personal touch, social skills and a sense of responsibility.

“If I were to add together the various perceptions of Swiss banks, the result would probably be just about positive,” says brand expert Stefan Vogler. The negative headlines of recent years have damaged the image of the Swiss financial centre – yet at the same time, regional banks in particular continue to enjoy a very good reputation.

Low confidence in the system offset by positive experiences

The latest Banking Monitor confirms the image expert’s assessment. Whereas 75% of the population viewed Swiss banks positively in 2021, the figure now stands at just 53%. At the same time, people’s satisfaction with their own bank remains high – at 83%. This reveals a deep divide between trust in the system and personal experience.

This divide can be explained by the different roles played by the various Swiss banks. “A regionally based retail bank is judged completely differently from a major bank,” says Markus Boss, CEO of Regiobank Solothurn AG.

He is often struck by the ambivalent image of banks in his day-to-day work: “Every day there are many thousands of positive interactions with customers, even though the public debate is sometimes dominated by negative issues.”

Proximity builds trust

According to Stefan Vogler, it is precisely these conversations with customers that are crucial to the positive image of local banks: “Banking is a business built on trust – and trust is built primarily through personal contact.” And in this respect, regionally based banks have an advantage over major banks.

Markus Boss reports that 95% of his staff live in the bank’s catchment area. This is where the regional bank really scores points: “We don’t just know the figures; we know our customers too.” Boss is convinced that the social skills of its staff are crucial to a bank’s success.

He was recently surprised to see for himself just how important the personal touch is. A customer opened an account worth around one million Swiss francs – not because of a product or a campaign. The deciding factor was that she had seen the bank manager with his son at a concert and found the way they interacted with each other endearing.

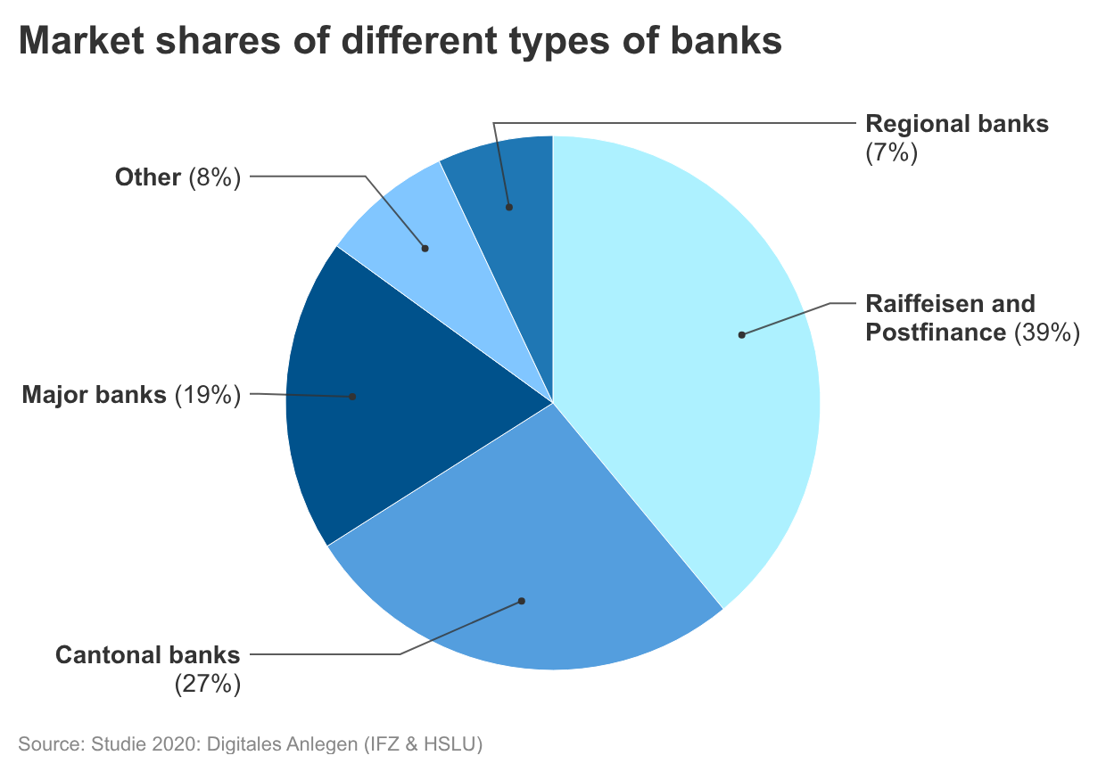

The various banks in Switzerland

Regional banks

Have strong local or regional roots and focus on private customers and SMEs in their region. Regional banks typically specialise in mortgages, savings and wealth management. There are 59 institutions, with an average of five branches per regional bank.

Cantonal banks

Are mostly owned by the cantons and have a public mandate to promote the regional economy. Many are backed by a state guarantee. They combine regional roots with a broader range of services – for example in investment advice, corporate banking or financing. There are 24 cantonal banks; only Solothurn and Appenzell Ausserrhoden do not have one.

Raiffeisen

A banking network comprising 218 regionally based and cooperatively structured banks. Raiffeisen banks focus primarily on traditional interest-bearing business, including mortgage and corporate loans, and customer deposits in the form of savings and investments.

PostFinance

The Swiss Post’s bank, which is strongly focused on serving private customers. With a broad network of post offices and digital services, PostFinance plays an important role in payment and account transactions.

Major banks

Following its takeover of Credit Suisse, UBS is the only major Swiss bank. It operates globally. In addition to traditional retail banking, international asset management, investment banking and capital market transactions play an important role.

Taking responsibility: attitude matters just as much as the balance sheet

However, customer focus and social skills alone are not enough to win people over. The Banking Monitor reveals that many Swiss bank customers believe the banking sector is neglecting ‘social responsibility’ and ‘sustainability’ issues.

Markus Boss understands that banks are judged not only on their performance but also on their attitude: “We manage money and advise on important decisions such as buying a house – naturally, we bear social responsibility.”

When it comes to sustainability, he sees banks’ primary responsibility as providing expert advice. However, he notes that the issue is driven by legislation and customers – and regarding the latter, he observes: “For most people, the return on investment ultimately counts for more.”

“Smaller, regionally rooted banks find it much easier to engage credibly and show social responsibility,” Stefan Vogler is convinced. Markus Boss himself serves as a good example of this. He was chairman of the local council in his home town until June 2025 and has been a member of the Solothurn Cantonal Council since last year.

Regional banks must be able to do everything

Smaller retail banks find it easier to win over customers personally. A competitive advantage – provided they manage not to fall behind other banks in terms of services.

Specifically, this means that regional banks must keep pace with the digitalisation of services whilst at the same time operating a counter offering personal customer service in every branch. “Implementing all these requirements is a huge undertaking – hats off to the regional banks for pulling it off,” says brand expert Vogler.