Switzerland as a business hub

No growth without market access: the Swiss financial centre in global competition

No growth without market access: the Swiss financial centre in global competition

Switzerland is known worldwide for its chocolate, the Alps and its banks. But whilst the Alps are unique, the financial centre must hold its own against emerging competition. To maintain its leading role in international wealth management, the banking centre is looking to new agreements.

“Competition is fierce,” says Denis Pittet, President of the Fondation Genève Place Financière, the umbrella organisation for the Geneva financial centre. For whilst Switzerland remains number one in international wealth management, other financial centres are growing faster.

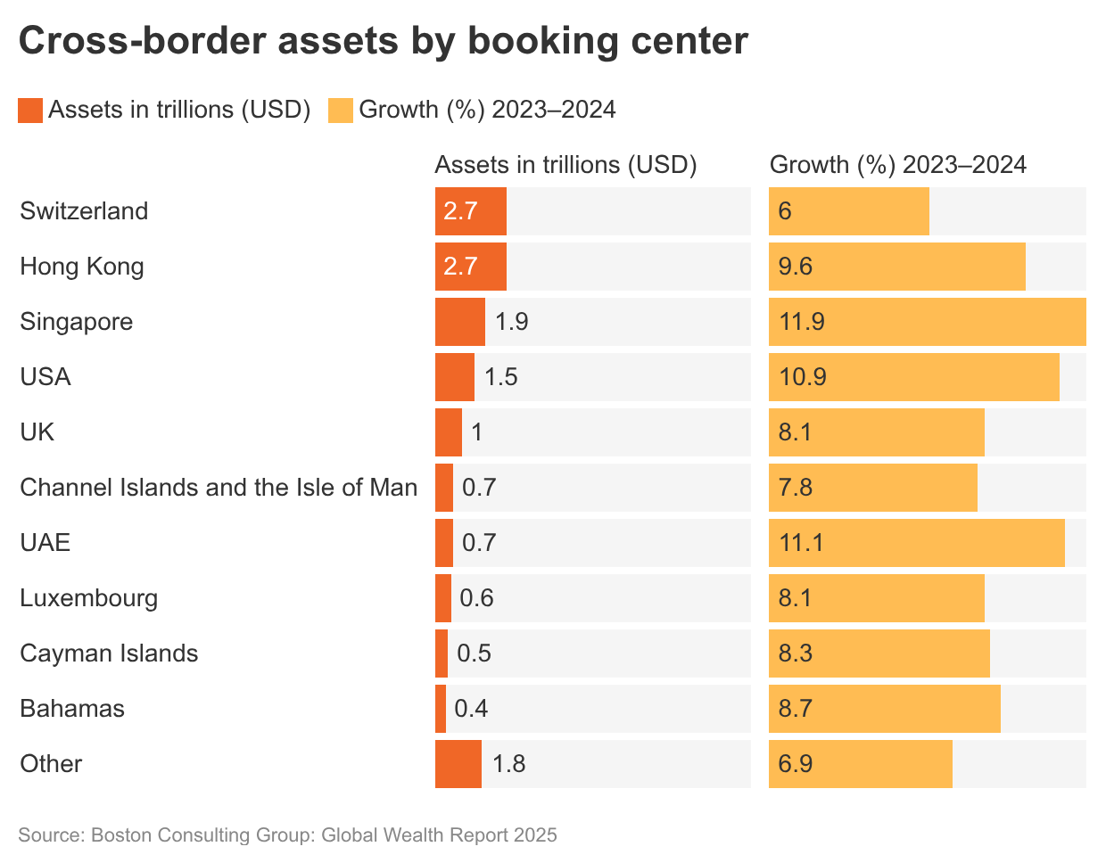

The Global Wealth Report 2025 predicts that Hong Kong will have overtaken Switzerland as the location with the largest international wealth management sector by 2029. Furthermore, between 2023 and 2024, growth in the other countries in the top 10 for wealth management exceeded that of Switzerland.

Banking activities abroad are growing, but there is a cost

At the same time, cross-border wealth management is losing ground globally. Its share of global financial assets fell from 5.3% to 3.7% between 2013 and 2023, as shown by the Deloitte International Wealth Management Centre ranking.

Conversely, the presence of Swiss banks outside Switzerland is growing in importance. Through their overseas subsidiaries, Swiss banks are also benefiting from the growth of foreign financial centres.

But Denis Pittet sees drawbacks to this form of expansion beyond Switzerland’s borders: “Jobs are being created outside Switzerland and tax revenue is being lost to our country.” The alternative – namely, international wealth management based in Switzerland – requires international agreements.

International agreements open up markets

An important step in strengthening international wealth management is the Berne Financial Services Agreement (BFSA) between Switzerland and the United Kingdom (UK). Since 2026, both countries have recognised each other’s legal and supervisory frameworks. This allows registered Swiss financial service providers to serve business and high-net-worth UK clients without having to obtain a UK licence – and vice versa.

For Pittet, a similar agreement with the EU is now needed: “We must establish a stable and long-term framework for relations with the EU.” This is because the EU is Switzerland’s most important foreign market: in 2024, over 60% of financial services exports were destined for Europe.

However, with the implementation of the EU’s CRD VI directive from 2026, market access has been restricted: core banking services may no longer be provided from Switzerland without a local presence. Investment services are now only possible to a limited extent – for example, for institutional clients or at the initiative of private clients (“Reverse solicitation”).

Talks with the EU

To gain better access to the European market, the Swiss Bankers Association is therefore calling for regulations based on a so-called institution-specific approach. Swiss banks that so wish should be able to place themselves under the supervision of a single European authority in return for being permitted to offer their services on the EU market. Consequently, only those Swiss financial institutions that are interested in this market would apply the EU requirements.

An obstacle course through the Bilateral Agreements

However, such an agreement is still a long way off. “Until we gain access, it’s an obstacle course – and the first hurdle is the Bilateral Agreements,” says Pittet. Still, the Bilateral III package was approved by the Federal Council in March 2026, bringing its implementation a step closer.

Although the package contains no provisions relating to financial services, rejection of the Bilaterals would likely prevent the conclusion of an agreement on access to the European market for Swiss financial intermediaries.

Furthermore, Pittet warns of indirect effects: without Bilateral Agreements III, Switzerland risks exclusion from education and research programmes such as Horizon Europe and Erasmus. This would weaken training and access to talent – with consequences for the banking sector’s competitiveness: “It’s like the Champions League: you can’t get by on local talent alone.”

Market access for economic growth

If, on the other hand, the obstacles can be removed and an agreement concluded with the EU, Pittet sees great opportunities for further growth: more jobs in the banking sector, greater competitiveness and additional tax revenue.

Today, financial services account for around 15% of total service exports – making it the second-largest export sector. Access to international markets will be crucial in enabling the financial centre to maintain, and indeed strengthen, its leading position.

The full interview is available in French on the podcast «Accès au marché européen : un accélérateur de croissance».