Switzerland as a business hub

No exports without banks: the invisible infrastructure behind Switzerland’s success

No exports without banks: the invisible infrastructure behind Switzerland’s success

Watches, coffee, gold and medicines – Switzerland’s success depends on the export of these products. But having a good product is not enough: exports also need to be financed and insured. Banks provide the necessary infrastructure for this.

The export of goods is a key pillar of Switzerland’s prosperity. Around 45% of gross domestic product is generated through the sale of goods abroad.

However, international business is complex: buyers and sellers often do not know each other, different legal frameworks apply, foreign currencies are an issue, and procedures take a long time.

To enable Swiss companies to offer their products and services worldwide, banks create the necessary framework for stable financing.

Liquidity as the lubricant of trade

Bank loans enable companies to accept orders without placing an excessive strain on their own liquidity. This is because international business ties up capital: months can pass between placing an order, production, dispatch and receipt of payment.

These are the most common reasons for taking out a loan: 1. for production (pre-financing loan/manufacturing loan), 2. as a bridging loan for the period between the conclusion of the contract or delivery and payment by the buyer (supplier credit or buyer credit and forfaiting).

Hedging against risks

A typical feature of this type of loan is that banks generally bear the risk of the buyer defaulting on payment – this is covered by private export credit insurance. The publicly funded Swiss Export Risk Insurance (SERV) exists to enable exports even to unstable countries. It also covers the risk of ‘force majeure’.

Particularly in the case of long delivery times, there is also the risk that the foreign currency will depreciate between the conclusion of the contract and payment, meaning the exporter receives a lower amount. Such falls in exchange rates can significantly reduce margins. However, companies can protect themselves against such losses, for example, by hedging the currency risk through forward foreign exchange contracts.

Trade relations require trust

In addition to the financial infrastructure, trust between trading partners is essential for successful foreign trade. Banks provide the necessary security here. Bank guarantees ensure that the exporter fulfils the contract, and letters of credit guarantee payment by the importer.

Furthermore, banks facilitate the expansion into new markets, as they possess local market knowledge and international correspondent banking networks. This support is particularly valuable when establishing new customer relationships – and is vital in times of geopolitical upheaval.

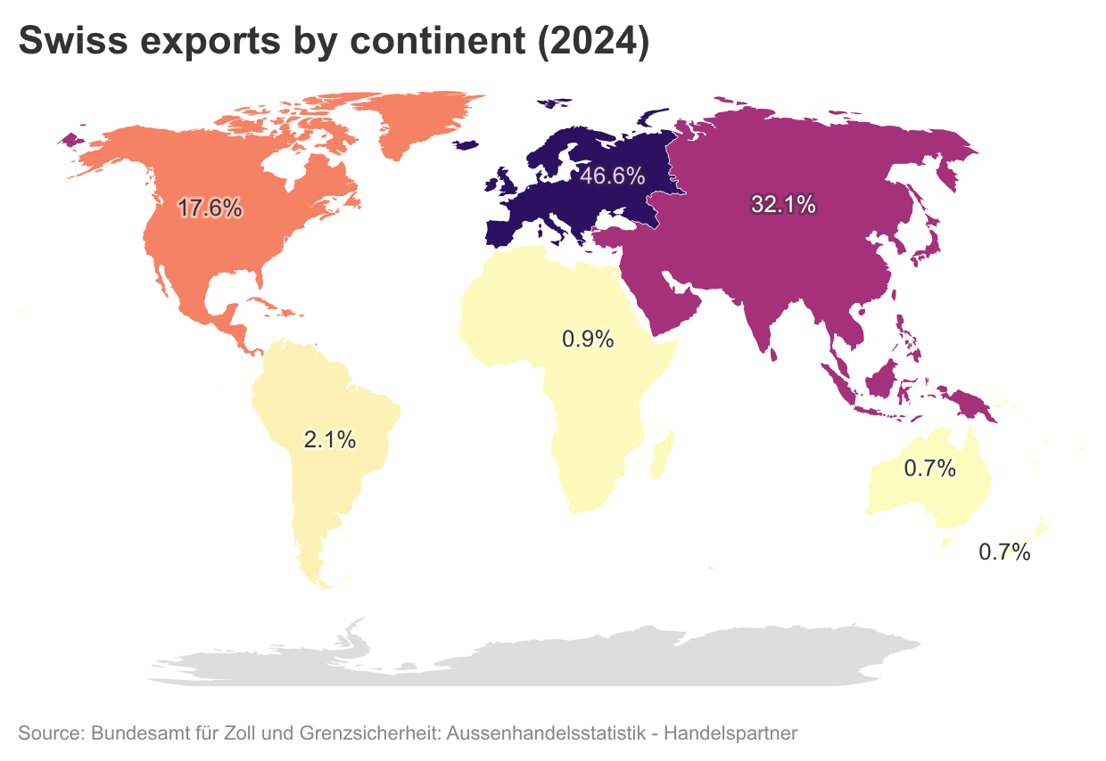

By 2025, trade conflicts with the US had led many Swiss SMEs to view South-East Asia and Europe as increasingly important markets, whilst the US was losing significance.

The whole of Switzerland benefits

The financing and security that banks provide for exports are particularly crucial for SMEs. Unlike large companies, SMEs often have lower financial reserves and lack their own currency hedging instruments.

Bank loans therefore act as an economic lever: they enable companies to generate more export revenue than would be possible with their own financial resources. This boosts gross domestic product and tax revenues, whilst intensifying the international exchange of technology and knowledge.

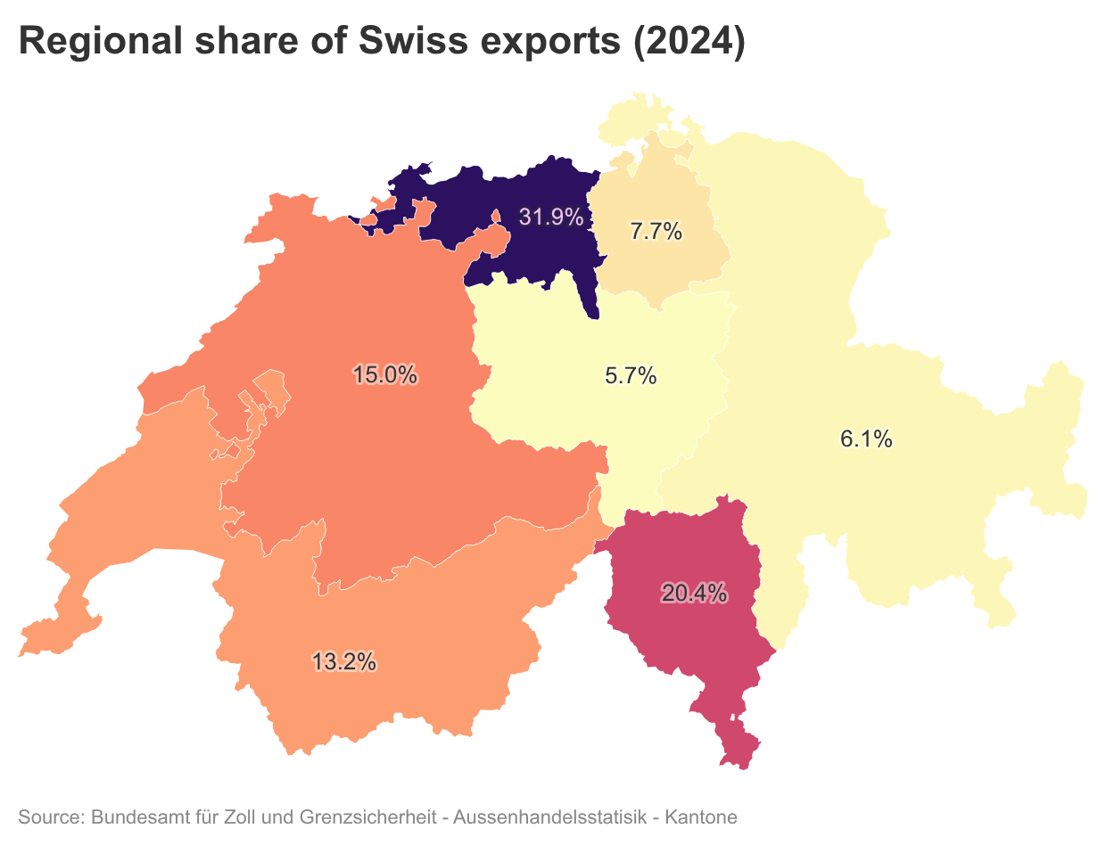

As SMEs account for around 40% of total export volume, export support benefits not only the Swiss urban centres where large corporations are based – but the whole country.